BLOG

California to Require IRC Section 1031 Taxpayers to Report Sale of Out of State Replacement Property

States Follow Federal Laws on Section 1031 Tax Deferral

While Internal Revenue Code (IRC) Section 1031 pertains to the deferral of tax on the federal level, the various states in the country generally follow the Fed's lead in this regard. So, if a transaction meets the requirements of IRC Section 1031, the state in which the relinquished property is located will similarly recognize the tax deferral. However, a few states take this matter of deferral a bit further and will only allow taxpayers who trade into replacement property in the state to avoid ongoing reporting. For those states, should a taxpayer acquire out-of-state replacement property, there is a requirement to pay to the state the original amount deferred when the out-of-state replacement property is sold. These state provisions allow the states to reach out into a future transaction and require the tax be paid upon the original transaction. Due to this ability to reach out and pull back the tax deferral, these state requirements are sometimes known as "clawback" provisions. States with clawback provisions include:

- Oregon

- Montana

- Massachusetts

- California

The State of California and the Proposed Form FTB 3840

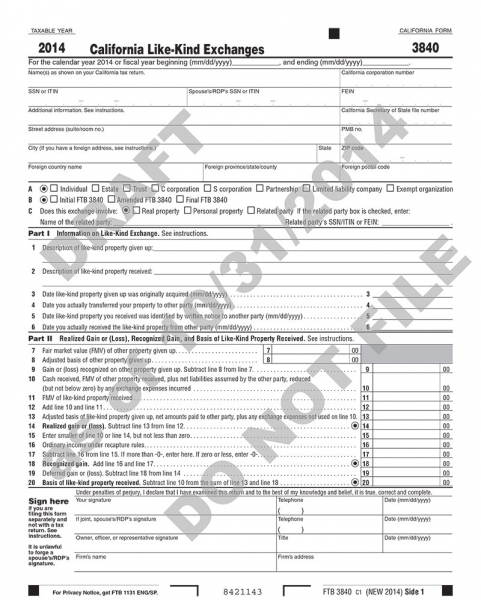

The State of California's Franchise Tax Board (FTB) has recently released a draft of its proposed form FTB 3840, California Like-Kind Exchanges, which would require taxpayers who sell relinquished real property in the State of California and who buy replacement real property out of that state to report annually the subsequent status of the replacement property :

The State of California's Franchise Tax Board (FTB) has recently released a draft of its proposed form FTB 3840, California Like-Kind Exchanges, which would require taxpayers who sell relinquished real property in the State of California and who buy replacement real property out of that state to report annually the subsequent status of the replacement property :

Form FTB 3840 must be filed for the year in which the exchange is completed and for each subsequent year until the California source deferred gain is recognized.

This form must also be submitted in the case of a multiple asset exchange that contains both real and personal property located in California for like-kind property located outside of California as described in the form instructions:

If personal property located in California was exchanged for personal property located outside of California as part of a single exchange that included California real property exchanged for non-California real property, combine each type of like-kind personal property given-up and report such personal property given-up as a separate property.

So if the status is that the property was sold in a subsequent year, the California tax will be recognized and paid at that time. In the case of a California resident who acquires replacement property out of state, the FTB 3840 is to be attached to the taxpayer's state tax return. For non-resident California state taxpayers, the requirement is for the taxpayer to file the form FTB 3840 as an informational return.

Sections of the FTB 3840 Form

Much of the form follows IRS form 8824, which is used to report like-kind exchanges on the federal tax return. The first section of the form seeks information on the like-kind exchange. The second section pertains to reporting recognized gain or (loss) and basis of like-kind property received. There is also some specific reporting required on a schedule to the FTB 3840:

- Part I - Information of Properties Given Up

- Part II – Information on Properties Received

- Part III – Information on Allocation of California Source Deferred Gain

Summary

Although the California form FTB 3840 is only in draft form currently and the State is requesting comments on the form, the state does intend to make it applicable for California like-kind exchanges taking place in 2014. This new filing requirement applies to all taxpayers, regardless of residence status or commercial domicile, who exchange real property located in California for like-kind property located outside of California. Non-California resident taxpayers who find themselves selling relinquished real property located in the State of California while acquiring replacement property outside of the state must keep in mind, and comply with this new reporting requirement.