BLOG

Reverse Exchange for Dummies

Reverse 1031 Exchange Rules

Under IRS rules for 1031 Exchanges, a taxpayer must sell the old property, the Relinquished Property, prior to acquiring the new property, the Replacement Property. However due to a wide variety of circumstances, a taxpayer is often faced with losing the opportunity to buy the sought after Replacement Property due to a potential closing date prior in time to a sale of the Relinquished Property. At times, the Relinquished Property is already under contract for sale, but the closing date is beyond the date of a Replacement Property acquisition time, or on occasion the Relinquished Property is not even up for sale or under contract yet. In those situations, taxpayers can utilize a Reverse Exchange.

What is a Reverse Exchange?

The term “Reverse Exchange” refers to a fact pattern where a taxpayer needs to effectively close on the acquisition of the Replacement property prior to the sale of the Relinquished Property. The funny thing is that the way to accomplish a Reverse Exchange is to restructure it so that it is not “reverse” at all.

In the year 2000, the IRS provided a set of rules providing a “safe harbor” for Reverse Exchanges when following those rules making it so taxpayers can do a Reverse Exchange. The term, safe harbor, basically means that the structuring of such a transaction is pre-approved by the IRS and will not be challenged as to the structure. To better understand a real-life situation in which a Reverse Exchange may be utilized review this Reverse 1031 Exchange example.

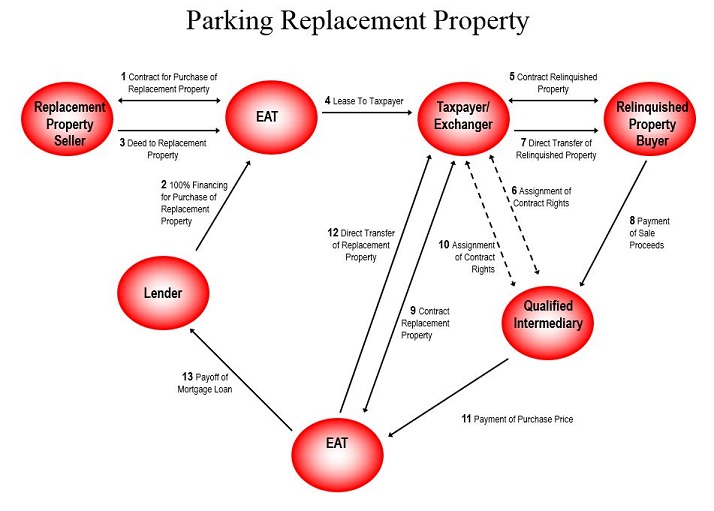

Reverse Exchange Process

Let’s look at how a reverse 1031 exchange works. The solution provided by the IRS is easier than you might imagine. Essentially the rules suggest under a reverse 1031 exchange process, a taxpayer can retain the services of an exchange company to act as an “Accommodator”, known in the regulations as an Exchange Accommodation Titleholder (EAT), to acquire the Replacement Property and hold it on the taxpayer’s behalf. Under these rules, the reverse 1031 exchange timeline provides that a taxpayer then has up to 180 days to sell the Relinquished Property and consummate the exchange for the Replacement Property being held. Since the taxpayer has not literally acquired the Replacement Property before the sale of the Relinquished Property, he has closed in the proper sequence. Perhaps a bit of smoke and mirrors, but who cares…, the technique is provided for by the IRS. Take a look at this Reverse 1031 Exchange diagram, for a comprehensive visual of the process.

{kind=link}

There are several steps to a valid Reverse 1031 Exchange, for a brief overview of these steps review the infographic.

Financing in a Reverse Exchange

In every deal, the question of how to finance the reverse 1031 exchange comes up. The Accommodator does not provide the funds for the purchase. That is done either by a loan from the taxpayer to the Accommodator and/or through a bank loan. That loan is paid back once the Relinquished Property is sold and those proceeds become available. Also, during the period where the Replacement Property is held by the Accommodator, it leases the property to the taxpayer effectively allowing the taxpayer to sublease the property to any actual property tenant and to collect and retain the rent. The taxpayer pays the utilities and other expenses per the terms of the lease. At the end of the day, the Accommodator just makes its fee, and all the economics are retained by the taxpayer.

Cost of a Reverse Exchange

Cost for a reverse 1031 exchange vary based upon a lot of factors. Such factors include the type of property such as residential, commercial, industrial, etc., the value of the property, and the source of financing, i.e., taxpayer funded, or bank financed. Sometimes there may be also be environmental issues to deal with which can affect cost. Remember, the exchange company is holding title to the property and the above considerations affect the cost.

Relationship of Reverse Exchange and Forward Exchange

People tend to be confused between the interplay of the Reverse Exchange and the related forward exchange. They often say, “Why do I need a forward exchange since I am doing (and paying for) a reverse exchange”. The answer is that although these both relate to a single overall transaction, they are separate, but necessary parts, to the whole transaction. As is now crystal clear to you, the reverse is being done to take the Replacement Property out of play and preserve your ability to trade for it. Technically a Reverse 1031 Exchange is not a 1031 exchange at all, better thought of as just a Reverse Exchange. The forward exchange is an actual 1031 Exchange where the Relinquished Property is sold and exchanged for the Replacement Property. Both are needed to complete a successful Reverse Exchange.

The forward exchange is serviced by a Qualified Intermediary pursuant to a different set of IRS rules than those for an Accommodator providing Reverse Exchange services. The Qualified Intermediary can be a single exchange company that is also wearing another hat acting as Accommodator, such as Accruit, or separate companies each providing services for just one type of exchange, but not both.

The material in this blog is presented for informational purposes only. The information presented is not investment, legal, tax or compliance advice. Accruit performs the duties of a Qualified Intermediary, and as such does not offer or sell investments or provide investment, legal, or tax advice.